Every so often our traders on the desk come across scenarios which can shape the financial landscape for many months, and offer some of the most fantastic risk:reward opportunities. These opportunities are not your average risk:reward scenarios – they are BIG PLAYS.

Often they are ‘hidden’ gems whilst at other times such plays are visible to all in the public. One such opportunity is happening before our eyes RIGHT NOW.

The longevity and perseverance of the European Union.

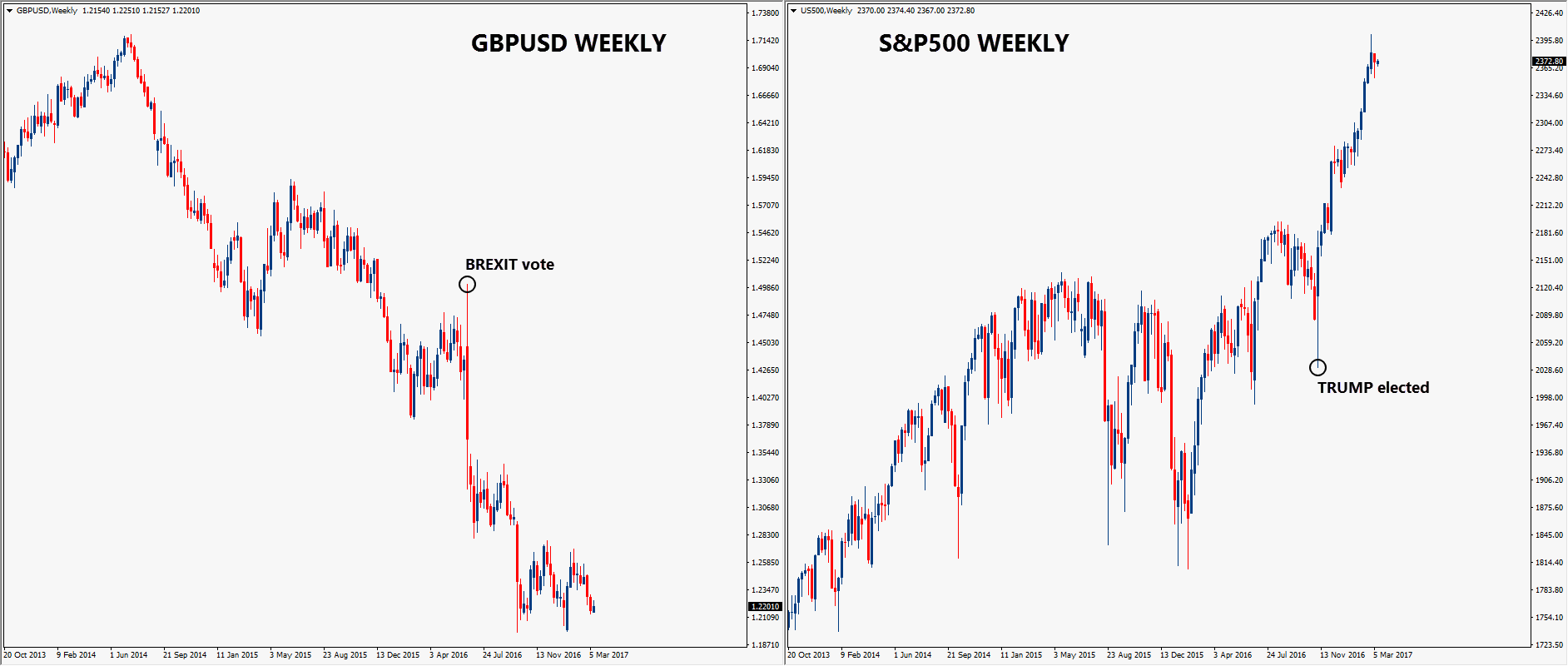

Since early 2016, members of our MEMBER PORTAL have been alerted to the rise of populism across the world and how this will affect the markets. The Brexit vote and Trump victory have encouraged a wave of anti-establishment sentiment – and the markets responded immediately:

The GBP took a serious hit, and global equities all jumped on board the Trump train:

Now, the question is….

How will European markets fair with this rise of geopolitical uncertainty?

This year we have three major elections across Europe, the first of which begins today.

Let’s take this opportunity to briefly cover the challenging nominees that may change the course of markets.

NOTE: As a firm we do not hold strong political views or affiliation to any parties.

2017 – A year of political uncertainty in Europe

Dutch Election – TODAY, Wednesday 15th March

By the time you have read this, the Dutch will be voting to elect a new Prime Minister of Netherlands. The right-wing populist Geert Wilders has in many ways been touted as the ‘Dutch Trump’ (although not by the Dutch!), with some very ‘strong’ views on border controls and EU membership. His claim is that in the long-term, there is a need for a ‘Nexit’.

Markets have been quiet surrounding this election, but our view is the outcome will be very important as markets gauge the future of Europe. We expect to see increased volatility over the next 24 hours with plenty of algo activity.

On these desk we are closely monitoring on this market and expect to see wild volatility as results filter through. The EURO may not see the same volatility, however we discuss what an upset result may mean below.

France Election – Sunday 23rd April (First round)

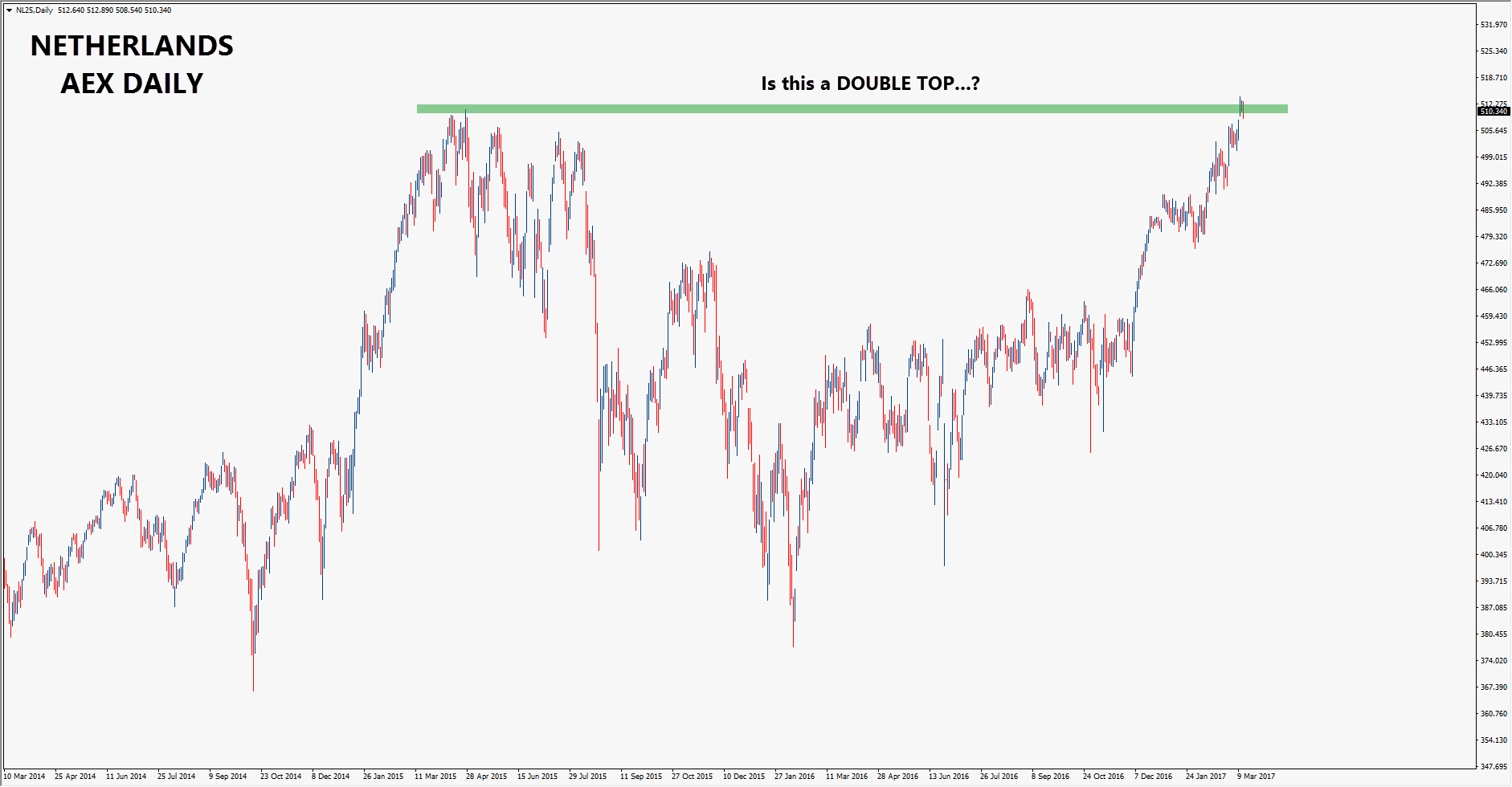

Overshadowing the Dutch election has been the 2017 Presidential Election of France. Like the US Election last year, we have seen quite a few twists however the local French market has remained set on a path to retest a very important area below.

From a systematic perspective, our models expect a break through this trendline followed by a retest, and ultimately resulting in higher prices moving forward.

Marine Le Pen is the far-right leader upsetting the establishment and like Wilders – see’s a future for France outside the EU.

It should be of no surprise why markets are paying attention to this election. France is the most popular tourist destination in the world, the largest country in the EU, and second largest economy behind Germany.

Over the past month we have noted Le Pen slipping far behind Macron, an ex-Investment banker and centrist hoping to reunite the country.

Will Le Pen become the first female president of France?

Or will we see a stronger EU with a win to Emmanuel Macron?

Our Head Trader believes that the French will vote for STABILITY

He likes investment bankers so Macron gets the vote =)

German Election – Sunday 24th September

Europe saved the biggest and best for last.

The immigration problem and ongoing Brexit talks has caused Chancellor Merkel some headaches, however yet again the markets have stood firm. Merkel is now being challenged by the ex-president of the European Parliament – Martin Schulz.

Unlike other EU countries Schulz was a fierce Brexit critic, suggesting the hardest Brexit possible for the UK. He is also the EU’s fiercest champion, even moreso then Merkel. To quote his is exact words:

‘With me there will be no Europe bashing’

Our head Trader Rob, a DAX enthusiast- believes that either way the DAX will benefit once the uncertainty fades. Again- higher prices to come.

Let’s recap why the European Union was established

As we all know the EU is an organisation comprised of 28 European countries, with roots tracing back to 1957 when the European Economic Community (EEC) was established.

This organisations founding members were France, (then) West Germany, Italy, Belgium, Netherlands and Luxembourg. They formed for the EEC primarily for the following reasons:

- To create stability within a region that had started two World Wars in 50 years (and many historical wars)

- Remove trade barriers between countries

- Establish a common market between participating members.

In 1969 – the same founding members then launched the EMU (European Monetary Union) to help facilitate the initiatives above.

10 years later, EEC governments establish the Exchange Rate Mechanism (ERM)- a mechanism that reduces volatility between Euro currencies, and ultimately sets undertones for a single currency market.

Finally – in 1999, the EURO is launched and trades at 1.1743 USD.

“As a desk when trading these Politically driven markets we will always look at both sides of the equation to understand what impact either conclusion has on our portfolio as a whole.” Robert Bubalovski – Head Trader

1 – Why the EURO will remain in-tact

It is blatantly obvious that the three reasons outlined above are critical to the peaceful and commercial prosperity of Europe. The European Union is indeed a visionary model for the continent as a whole. It enforces rules, standards, and transparency across all markets.

There is also alot standing in the way of Le Pen and Wilders (should they win) requesting to exit the EU. A win to either will unlikely translate into a majority house win. Additional no other local parties are fond or willing to work with them so forming a coalition government may prove difficult. And without this majority – EU referendums in these countries are

Take for example:

- France’s constitution says it is part of the European Union.

- Therefore it will need a constitutional change to exit the EU.

- Changes to the constitution must be proposed by the Government, NOT the President.

Adding to this, there are other countries in Europe that are still waiting to join the EU. Put simply – the EU provides many advantages to countries that can adhere to its policies.

To date – we must consider that the Euro currency is still ‘business as usual’ despite years of tumultuous events. It has been through crisis after crisis since the GFC, and the EURO is still irrespective of bad news.

We have said this before – when all the bad news is on the table (and the market hasn’t collapsed), there’s only one way for the market to go!

2 – Why the EURO is doomed to fail (if there is no reform…)

One of the major issues with the EURO is the centrally imposed monetary policy by the ECB. That is- one monetary policy (one interest rate) across all EURO adopted countries. This has caused major financial strains across Europe as each country is still obviously responsible for their own fiscal policies (i.e national budget, taxation etc).

Another issue surrounds the output and productivity of Euro countries.

Germany and France are Europe’s biggest producers and therefore the EU’s biggest proponents and contributors. However smaller countries such as Greece, Portugal and Ireland have struggled to adhere to the EU’s policies.

Many argue that the once unifying European model is now turning, as governments are not at the liberty to seek changes for their country under membership; and thus contemplating to leave.

If one Euro country did vote to leave (especially one of the founding countries), markets would immediately begin to speculate on another country leaving. This would cause huge instability across the region and for the EURO currency.

Governments who held such a country’s debt would also incur significant losses, causing further political instability and we would undoubtedly see bond prices (of the nation exiting) spiral out of control.

This would result in a significant EURO currency sell-off, and we may see other asset classes correlate to this, as capital flows would certainly move out of Europe. This is an important consideration as higher correlation makes diversification increasingly difficult.

We can see that everything above goes against this wishes of European nations wanting stability.

Conclusion – Looking forward to the months ahead

From a macro perspective, it is in the best interests of all markets for the EURO stay resolute. Quite simply – the EURO was established to provide unification amongst Europeans in many ways – from borders to commerce, to financial markets.

Think about this for a second – Germany is the largest economy in Europe – as a smaller country who has struggled with it’s own policies would you not look up to Germany and say to yourself :

“These guys are doing the right thing, maybe we should follow their lead”

Then there is ongoing saga that is Brexit-

Britain has yet to invoke Article 50 (required to begin negotiations on a UK exit), however the markets continue to price this with sharp declines in the GBP/USD.

With all the uncertainty across Europe, we are seeing opportunities for substantially large moves across European markets – particularly in the EURO and GBP crosses, as well as the Major European Indices and Bonds.

ARE YOU READY to take advantage of these scenarios?

If you want to know more, see some of our proprietary analysis feel free to comment below or contact us now!